Fannie and Freddie in 2025 - Part 1

The Trump Administration considers re-privatizing the mortgage giants while still keeping the government guarantee on the companies.

In the past few weeks, the topic of what to do with Fannie Mae and Freddie Mac has returned to the financial policy front burner. If you are a mortgage bond nerd, this will be interesting and vital news to you. If instead you are a normal person, the Fannie and Freddie debate might not have broken through your daily news stream of the world burning.

As a lifetime member of the former group, I’m quite interested in Fannie Mae and Freddie Mac news.

In this post and others to follow, I argue that

This is a big deal for the housing market and homeowners, US taxpayers, and the US government. These two companies guarantee 50% of mortgage-backed securities, with a notional value of $6.6 trillion. We should all pay some attention.1

The past and current situations of Fannie and Freddie - previously known as Government-Sponsored Entities (GSEs) are unique artifacts of the 2008 financial crisis, again worth knowing about.

What happens next, which for the first time in more than a decade has begun to take shape, is quite important for the future of homeowners, taxpayers, and US government finance. I’ll mostly get into “what happens next?” in Part 2 and Part 3 posts.

This post will be mostly history and updating and “how did we get here?”

The recent (since 2008) past of Fannie and Freddie

Technically the two mortgage bond giants have been in a “conservatorship” of the federal government, specifically their regulator the Federal Housing Finance Agency (FHFA)2, since September 2008. A conservatorship is kind of like bailout/bankruptcy but with a government agency as the trustee. '

That all happened because these mortgage giants experienced losses on their mortgage bond portfolios they owned, and on the mortgage bonds they guaranteed, and they were massively leveraged going into the summer of 2008. They were the ultimate “Too Big To Fail” financial behemoths that also play(ed) essential roles in the plumbing of mortgage and housing finance. It was good they got “conserved,” because - like a number of big finance companies (with the exception of Lehman)3 - their implosion would have caused unwarranted and uncontrollable collateral damage.

A simple version of the 2008 conservatorship (bailout) deal said:

The federal government backstopped their debts and their role as insurers to mortgage bonds. This was a bailout of Fannie and Freddie as companies, but also more importantly a bailout of all the mortgage bond investors and financial institutions who depended upon the guarantee of Fannie and Freddie.

The federal government obtained warrants which gave it the rights to own, at any time, 79.9% of the common shares of the two companies. That option has not been exercised yet, but it gives the federal governments ownership of 80% of the common shares of these companies whenever it wants. The warrants are good until September 2028, so the future of Fannie and Freddie after conservatorship is likely to be sorted before then.

The federal government also obtained $100 billion of senior preferred stock that the companies had to pay 10% interest on. Between 2009 and 2011, the companies couldn’t afford to pay this 10% on their initial $100 billion in preferred shares to the government, so the Treasury authorized an additional up-to-$200 billion more in senior preferred stock, of which only a portion was drawn on by Fannie and Freddie in those years. This senior preferred stock has an interesting feature that under ordinary circumstances should have left regular common shareholders permanently wiped out4, that requires further explanation.

Because the companies could not afford to pay the interest they owed from 2009 to 2011, the Obama administration made an amendment to their 2008 deal. The new deal was that all profits from these businesses would be sent to the US Treasury, in perpetuity. This became known as “the sweep” because profits were swept every year into Treasury. This was fair because the companies weren’t profitable enough between 2009 and 2011 to match their basic obligations, so the new deal was “since you can’t pay us what you owe, pay us everything you can.” If the companies earned $10 billion a year in profit for example, the amount they are obligated to pay Treasury increases by $10 billion. As of Q3 2024, the amount owed to Treasury to satisfy the senior preferred shares stood at $340 billion. That number, $340 billion, is worth remembering for Part 2 of this series.

Also and interestingly in 2012, the companies became profitable. Between 2012 and 2019 they paid back all the money they had initially borrowed, plus interest, such that taxpayers have earned an 11.6% IRR on funds received. The $340 billion is still outstanding, but taxpayers have already earned a healthy positive “profit” on the money invested in the GSEs.

Movement in shares of FNMA (Fannie Mae) and FMCC (Freddie Mac)

The companies may not pay dividends to common shareholders. To the extent the companies have profits, their payment obligation to Treasury increases to exactly capture all of their profits. The permanent obligation to pay all future profits to Treasury would normally imply that common shareholders of FNMA and FMCC are wiped out, worth zero. But that’s not the end of the story.

As you can see from the charts below of Fannie and Freddie shares, something else has been happening over the past 5 years, and in particular over the past 7 months.

Throughout the first Obama administration, Fannie Mae was a penny stock, trading under $1. After that, between the second Obama administration and the first Trump administration the stock traded between $1 and $4 on speculation that one or another change to the terms of the conservatorship might someday benefit common shareholders. The stock returned to penny stock status under the Biden administration 2021 to 2024, but then leapt after the November election of President Trump to over $1. In 2025 and in particular in response to Trump’s recent public musings, the stock has soared. Fannie Mae now has a $10 billion capitalization compared to around $1 billion a year ago.5

Above is the picture of Freddie Mac shares, which closely mirrors Fannie Mae’s move from penny stock (under $1) to something much larger after President Trump’s election in November.

The same preferred shares deal is still in place.

However, an important change happened in January 2021, just before the end of the first Trump administration. The companies were allowed to retain their profits and not send them to the US Treasury. The sweep was ended and the result was that the companies have increased their capital.

Even though they may retain their profits under conservatorship, they still technically owe all of that amount to the US Treasury. Which is weird, but that’s the current deal without a formal change in policy. They make about $25 to $30 billion per year, which they now retain but that also increases their ultimate amount owed to Treasury.6

What do the GSEs do?

Although Fannie Mae was first Congressionally chartered during the Great Depression to provide home loan liquidity, the GSEs evolved into shareholder-owned for-profit companies with an implicit government guarantee and an explicit rejection of any government guarantee.

The companies’ primary business evolved to provide insurance to mortgage bonds. The way a mortgage bond works is that you can put a thousand mortgages7 into a structure that collects a thousand different (diversified) home-owners’ monthly principal and interest payments. The bond structure then regularly pays out that money (minus some servicing and insurance fees) to mortgage bond investors. If some dozens of individual mortgages default for a little while, or entirely, the GSEs will act like an insurance policy to make up the difference to bond investors, who will never notice any change. That’s the insurance part, replacing potentially lost payments to bond investors.

The GSEs currently get paid in two ways. First, they charge a small insurance premium to guarantee any late or defaulted payments. Next, they can take over individual defaulted mortgages and do workout plans, which can lead to recovering funds through foreclosure or restoring the mortgages. Because the majority of mortgages have some home equity protection, and the vast majority of mortgages do not fail, this is a relatively low-risk business for the GSEs.

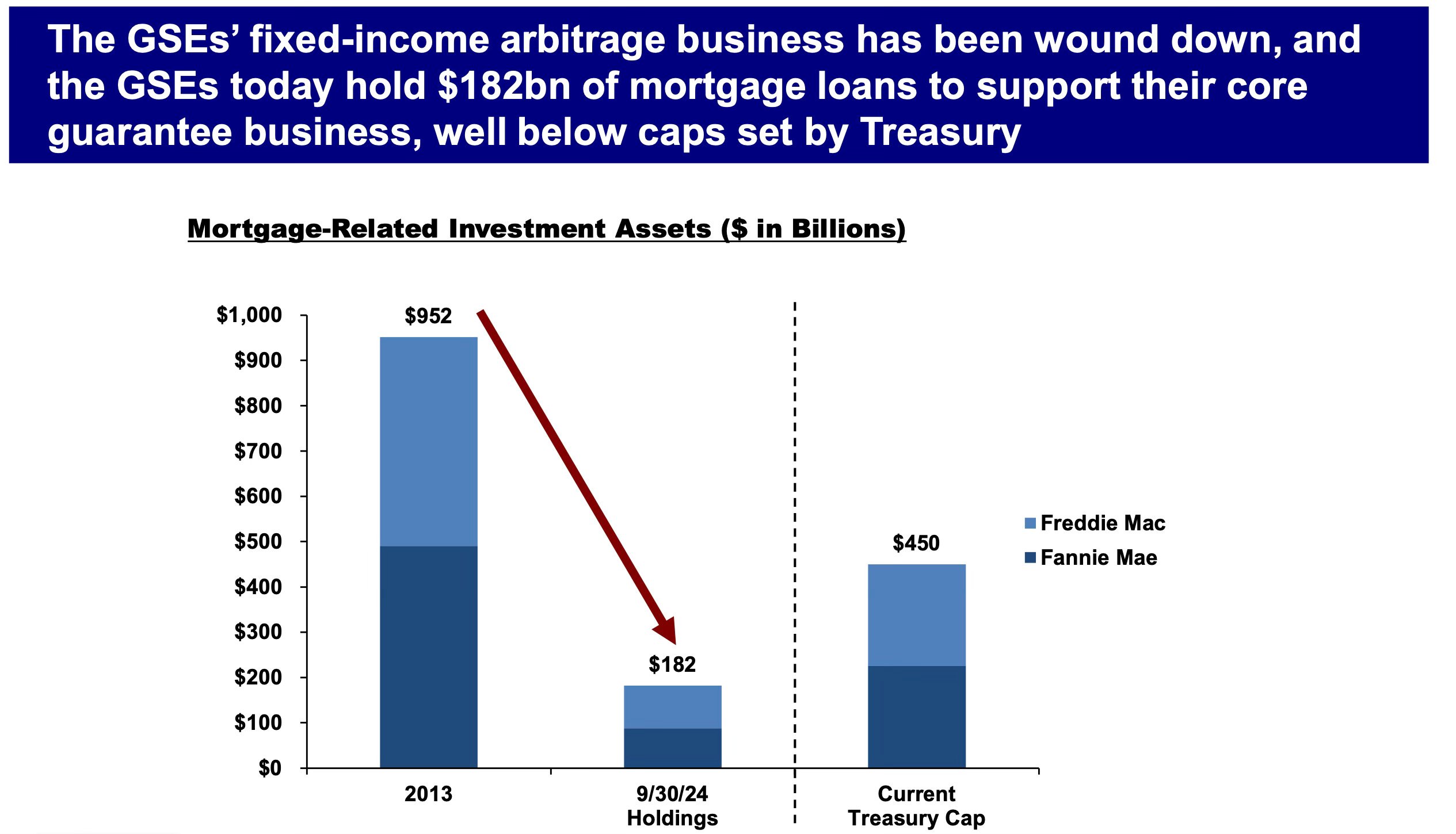

A secondary business that the GSEs have traditionally been in is buying up mortgages and mortgage bonds, and financing the purchases through issuing debt. (What is referred to in the graphic above as the “fixed-income arbitrage business.” This made money historically because the GSEs could borrow money at a lower interest than what they could earn through owning mortgages and mortgage bonds. It also explains why they got too big. Warren Buffett described this line of business in 2008:

“…[T]he portfolio operations enabled both of those entities to use, in effect, government-related borrowing costs and sort of unlimited credit, to set up the biggest hedge fund in the world...So the portfolios are poison. They aren’t really needed to carry out the function of Freddie and Fannie.”

I think that is basically right. The bond insurance business is good and useful to the US housing market and, done right, is probably low risk. The portfolio expansion side (aka “fixed-income arbitrage” side of their business,) however, using unlimited credit, got too big and too risky. It was profitable for a long time, which is why CEOs of a private shareholder-owned company would want to do it, but it was also their undoing.

By 2025, under government conservatorship, they have shrunk the portfolio-owned business to one tenth of its former size, which is good. Meanwhile, the two companies combined still earn insurance-style income on guaranteeing mortgage bonds, to the tune of about $30 billion in annual profits. After 2012 they became cash cows for the US Treasury, and since 2021 they have retained their cash to build up capital, probably with the intention of ultimately leaving conservatorship.

History of GSE (pre-2008) - public and private hybrid features

Fannie Mae and Freddie Mac existed for decades in that liminal space between public and private companies. Created by Congressional mandate, and as such labelled Government-Sponsored Entities (GSEs) they nonetheless evolved to act like private companies, with the trappings of a private enterprise such as freely-traded shares, a shareholder focus on profitability and growth, and highly compensated CEOs.

Important distinctions existed between them and private financial institutions, however.

For one, although the GSEs were government-birthed, their investor disclosure documents historically pointed out that they were specifically not government guaranteed. This is an extremely important distinction and issue in the history of the GSEs, which I’ll get into in Part 3 of this series.

And yet, investors always understood the GSEs to have in implicit (but explicitly not explicit!) government guarantee. It was this implicit backing that made certain folks favor them for years, all the way up until 2008, when the crisis forced the implicit guarantee into an explicit backstop and bailout.

Buffett, Munger, Greenspan

Warren Buffett understood the power of the implicit government guarantee when he used to brag about owning Freddie Mac. In the 1980s his partner Charlie Munger was quoted saying ''I can't think of a more tangible compliment to the stock than to buy every damn share we are allowed to,” and explained his reasoning in an 1988 investor letter when they owned about 9% of Freddie Mac.

These guys knew a good thing when they saw it. They (and other investors) got private market-based rewards with low government-based risk. That's…nice.

But also, obviously, this hybrid situation was a preview of the kind of thing which made people (like me) extremely angry about how the whole 2008 crisis went down. You had market-based rewards (portfolio gains and generous executive bonuses) in good years and government (or socialized) losses in bad years. It was enraging. The GSEs were set up and operated that way for decades, all the way until their nationalization in the Fall of 2008.

Former Federal Reserve Chairman Alan Greenspan, no anti-markets socialist, in the years before 2008 had argued that Fannie and Freddie should be nationalized. This was based on the fact that they took increasing risks based on their implicit government guarantee. As long as investors thought the federal government backed the companies, they could borrow more cheaply than anyone else, and take more leveraged risks than anyone else.

At the very least, he argued, they should be more tightly regulated and limited in their size.

And then there’s Buffett and Munger in this video on Freddie Mac in 2001, explaining why they had entirely sold their position. Neither he nor Charlie Munger specify in the video what exactly they were worried about, but probably it was in part the move by both companies toward lower-credit mortgage guarantees. They say they were not concerned with government regulation in the case of the GSEs, but “rather the opposite,” which put them in line with Alan Greenspan’s view. They thought the companies were on the wrong track, and they thought regulators should more tightly control them.

Another feature of the hybrid public/private nature of the companies was that - again because the GSEs were birthed by Congress - important power-players in DC always believed that had a right and obligation to give political assignments to the GSEs. If Washington wanted to increase the percentage of homeownership among American households, then the GSEs would be given a mandate/instructions/moral suasion to make that happen.

In retrospect, the push into sub-prime lending pre-2008 by Fannie Mae and Freddie Mac looks terrible. But it was in some important way a political directive to increase the blessings of home ownership on a wider array of lower-income and lower credit-scoring families. Private banking companies also fell all over themselves to increase sub-prime and low documentation lending in the 2001 to 2007 era, but Fannie and Freddie were doing it in part for political, government-mandated, reasons.

This historic hybrid public/private nature of the GSEs explains

Why they got so incredibly big

Why Wall Street kind of always assumed the government would bail them out if necessary

Why they got into sub-prime and lower credit lending despite the known risks.

Right now they are fully publicly-owned in the form of the conservatorship, but that’s increasingly likely to change in the next 1 to 3 years.

I’ll discuss in a Part 2 post the outline of terms being considered by the federal government to re-privatize Fannie and Freddie.

This Bloomberg story by Matt Levine is a great primer, one of at least three that he has written on the topic.

The FHFA replaced the previous regulator OFHEO (The Office of Federal Housing Enterprise Oversight) in 2008.

I say “with the exception of Lehman” because that’s the big one that actually did cause uncontrollable and unwarranted collateral damage. I’m pretty sure the Lehman bankruptcy is the one Too Big To Fail company which the Treasury and Federal Reserve wish they had not allowed to fail in such an uncontrolled way.

This is a key interesting thing upon which “what happens next” depends! For more on that, see upcoming Part 2!

The path of Freddie Mac is quite similar, with just smaller numbers when it comes to stock price and ultimate market capitalization.

Which again stood at roughly $340 billion in 2024.

I have just picked a thousand mortgage as an arbitrary number of mortgages that go into a mortgage bond. It could instead be hundreds or it could be thousands. The raw material mortgages will typically have similar characteristics like a tight range of interest rates, similar underwriting/issuance date, and a similar maturity (typically 30 years or 15 years, but other variations can exist). Most bonds are made up of geographically diverse mortgages and have a range of sizes, but mortgage bonds can also be constructed out of a concentrated geography (all California mortgages for example) or all jumbo (large size) or all small-balance mortgages.